Medicare Supplement Insurance is an optional supplemental insurance coverage that can help pay for medical expenses not covered by Medicare. It’s also known as Medigap or medical gap coverage.

Medicare supplement insurance, like https://www.medisupps.com/medicare-supplement-plans/, provides reimbursement to you for some or all of the costs of health care services that aren’t covered by Medicare Part A, B, C, and D. You may need it if your health care costs are higher than those typically paid by Medicare, including hospitalizations and nursing home stay.

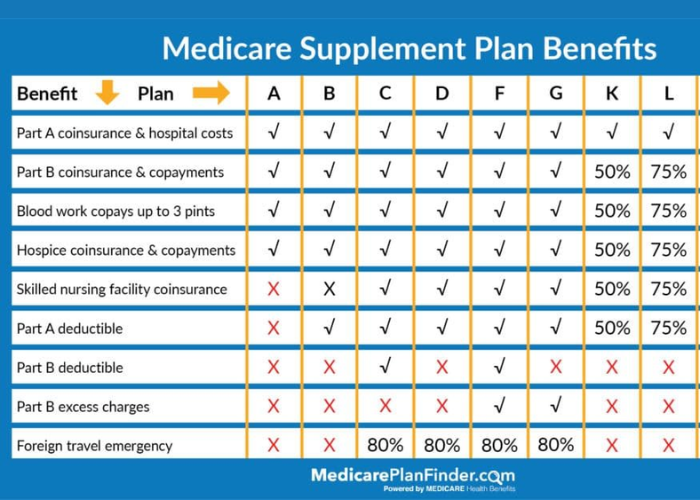

Medicare supplement insurance policies differ among states and counties but typically have similar features. The most common types of procedures include:

Network Preferred Provider Organization (NPPO)

A network preferred provider organization (NPPO) is a Medicare Supplement insurance policy that allows you to choose your doctor or other medical provider.

An NPPO can be considered an “insurance company” that benefits people who do not have Medicare. The provider must be in the insurance company’s network, and all of the doctors in that network must accept the plan’s formulary, which means they will only accept Medicare payment for their services.

There are two types of NPPOs: Preferred Provider Organization (PPO) and Health Maintenance Organization (HMO). PPOs require you to see a primary care physician within their network; HMOs require you to see a primary care physician within their network but also have some flexibility when traveling outside the area covered by your provider.

Health Maintenance Organization

Health Maintenance Organizations (HMOs) are voluntary managed care plans that provide their members with a wide range of medical services. They are typically the most expensive Medicare Supplement plans available, and may not be suitable for everyone.

A Health Maintenance Organization (HMO) is a Medicare Supplement plan offering an integrated network of doctors, hospitals, clinics, and other providers in one provider network. This can be a good choice if you have health issues requiring more than one specialty physician or hospital, or need access to special services like substance abuse treatment in your local area.

Ongoing care is provided through the HMO’s network of providers. You can go anywhere in the HMO’s network for consideration if it isn’t outside the geographic area covered by the HMO’s contract with Medicare. The primary difference between an HMO and traditional Medicare Supplement plans is that there is no out-of-pocket cost for medical services until you reach your annual deductible. After that point, you pay coinsurance based on how much your expenses were for the year.

Point-of-Service (POS)

Point-of-service Medicare Supplement insurance policies are designed to provide supplemental coverage for Medicare benefits. These plans are typically offered by a private insurer and purchased through your employer or the government. They can be purchased as stand-alone policies or bundled with other health coverage, such as dental and vision plans.

They are similar to traditional Medicare supplement policies but do not cover all the same benefits. For example, POS plans do not cover hospitalizations or reimburse you for doctor visits or outpatient services like physical therapy. In addition, POS plans do not cover prescription drugs or home health care services. Other than these differences, POS policies offer the same level of protection as traditional Medicare supplement policies.

Ultimately, your primary care physician will offer you an option better suited to your needs. As more companies begin offering benefits to Medicare supplement plan holders, you have more options when selecting something new if you feel like there’s a better fit, like medisupps.com/medicare-supplement-plans.